Turning Open Banking Data into Affordable Loans for Thin File Borrowers

Koyo Loans was the UK's first open banking-mandated personal lender, serving the 6 to 8 million Britons with thin or no credit files. Scaling a fintech lender that rejects bureau-only scoring required precision targeting and relentless conversion work. We ran paid acquisition, landing page optimisation, and full-funnel measurement to drive funded loan volume at sustainable unit economics.

A VC Founder's Credit Gap Became a Fintech Mission Serving Millions

Thomas Olszewski, a former venture capitalist at Frontline Ventures, founded Koyo Loans in 2018 after immigrating from the USA to the UK and discovering firsthand how thin credit files locked newcomers out of affordable borrowing. His product targeted the 6 to 8 million Britons with no or minimal bureau data from Equifax, Experian, or TransUnion, people who otherwise faced payday lenders charging over 1,000% APR or guarantor products at 50 to 99% APR from the likes of Amigo Loans and 118 Money.

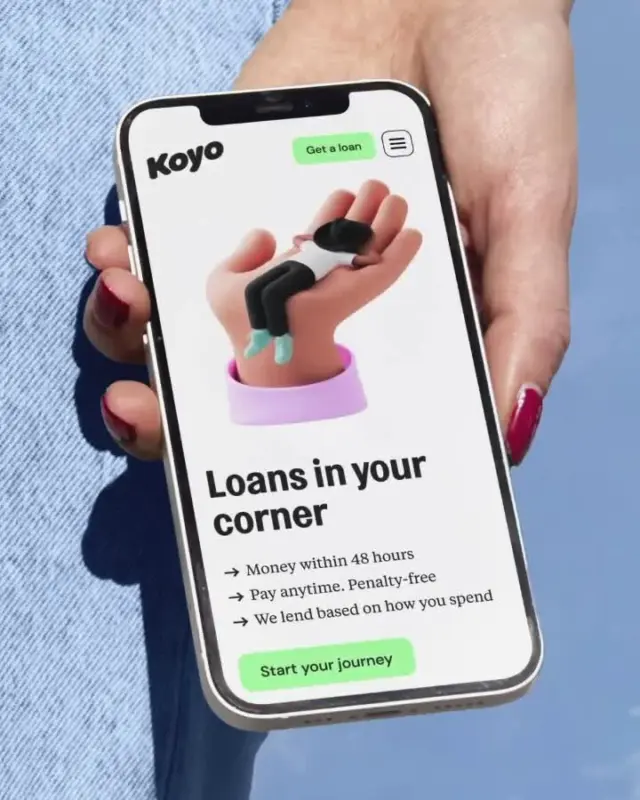

Koyo mandated open banking connections for every applicant, analysing real-time transaction data to assess income regularity, spending patterns, and affordability. This enabled a representative APR of around 35%, with zero late fees, origination fees, or early repayment charges. Backed by a $4.9 million round from Forward Partners, Seedcamp, and angels including LendInvest founder Christian Faes, the company launched in 2020 with a six-person team including CTO Guy Evans and Head of Risk Kevin Allen. Koyo asked us to build a paid acquisition engine and conversion pipeline that could deliver funded loans profitably in a market where fintech CAC averaged £200 to £500 per loan.

Targeting Underserved Borrowers Against High Street Banks and Guarantor Lenders

Koyo competed for thin-file borrowers against guarantor lenders like Amigo Loans and 118 Money plus high street banks like Lloyds and NatWest. We chose Google Ads to intercept active loan seekers and Meta to build awareness among 18 to 34 year olds and migrant communities who overindex on app-based finance. On Google, exact match captured high-intent queries while broad match with in-market audience signals expanded reach affordably despite £10 plus CPCs on finance keywords. Meta exclusion audiences filtered out existing credit holders, concentrating spend on genuinely underserved borrowers rather than those already served by bureau-scored products.

Pre-Qualification Forms Engineered for Funded Loans Not Just Completions

The gap between pre-qualification starts and funded loans was Koyo's critical conversion bottleneck. We A/B tested form length, field sequence, and progressive disclosure against funded loan rate rather than form completion. A three-step layout with open banking consent surfaced on step two filtered applicants unlikely to connect their accounts, improving downstream conversion. Placing the 35% representative APR above the fold alongside a 'no fees ever' trust badge lifted pre-qual starts by 22%. Mobile page speed was optimised to under 2.5 seconds since 60% of traffic came from mobile devices, consistent with the thin-file demographic's preference for app-based finance.

Measurement That Tracks to Disbursement Not Application Volume

Most fintech lenders optimise to application volume and lose sight of funded outcomes. Beyond the offline conversion loop feeding bid algorithms, we built a Looker Studio dashboard giving Koyo's team direct visibility into cost per funded loan, pre-qual to funded conversion rate, and average loan value by channel, campaign, and audience segment. Weekly reporting cadence let us shift budget within 48 hours when funded loan rates diverged from application signals. This measurement discipline, tracking all the way to disbursement rather than stopping at form completion, drove the 34% reduction in cost per application and ensured scaling spend never outran unit economics.

Bidding on Thin File Intent Where Bureau Scores Cannot Reach

We structured Koyo's Google Ads around a three-tier match-type architecture. Exact match captured high-converting thin-file queries like 'loans for no credit history UK' and 'personal loan without guarantor.' Phrase match expanded into affordability-adjacent terms such as 'low APR personal loan' and 'no fee loans.' Broad match ran with tight in-market audience signals layered from open banking adoption demographics and age filters for 18 to 34 year olds. On Meta, we built lookalike audiences from Koyo's funded borrower data and segmented by migration interest proxies, behavioural signals for app-based financial products, and negative exclusions for established credit profiles.

The decisive technical layer was server-side integration between Koyo's loan management system and Google Analytics 4, passing funded loan events back as offline conversions to Google Ads Smart Bidding and Meta's Conversions API. This meant algorithms optimised toward actual disbursements, not form completions. Budget allocation shifted weekly against a cost-per-funded-loan target, which inverted the typical fintech approach of optimising to cost per application and hoping downstream metrics follow.

Six Thousand Pre-Quals a Month Rewrote the Open Banking Acquisition Playbook

The engagement delivered a 21% lift in funded loan volume and cut cost per application by 34%, while scaling to 6,000 monthly pre-qualification starts. These results demonstrated that thin-file lending could sustain profitable digital acquisition when measurement extended beyond click metrics to actual loan disbursement. We proved that pre-qualification form design matters more than ad creative volume in financial services, because the gap between a started application and a funded loan is where most spend leaks.

The thin-file opportunity in the UK remains substantial, with 7 million consumers still underserved and open banking adoption now exceeding 10 million users. Variable recurring payments under FCA mandates will enable embedded lending directly within current account apps from providers like Starling and Monzo, creating distribution channels that bypass traditional paid search entirely. AI-driven risk scoring is reducing defaults by 15% according to McKinsey, but FCA scrutiny of algorithmic bias in lending models means that transparent underwriting, exactly Koyo's founding principle, becomes a regulatory advantage as much as a product differentiator.